A Forensic Look at Tootsie Roll Industries (NYSE: TR)

Tootsie Roll’s safe image hides red flags, weak capital allocation, and a valuation 3x above intrinsic value.

I originally began researching Tootsie Roll Industries (TR) with the intention of writing a traditional investment thesis — the kind I usually publish when a company looks undervalued or misunderstood.

But as I dug deeper into the financials, management behavior, and accounting policies, something didn’t sit right. The company’s narrative — conservative, long-term, shareholder-aligned — didn’t match what the numbers and disclosures were telling me.

So instead of forcing a thesis where none exists, I decided to share this research as a commentary — a case study in how a beloved, “safe” business can mask serious red flags behind a strong brand and a clean balance sheet.

I think it’s a useful reminder of why it’s so important to go beyond the surface when analyzing any company. Strong headlines and legacy brands aren’t enough. When you look closely at capital allocation, incentive structures, and cash flow quality, you often see a very different business than the one being marketed.

So, TR is a smallcap confectionery company that’s been in business for over a century. Its brands — Tootsie Rolls, Tootsie Pops, Dots — are American classics, and the company prides itself on “long-term thinking,” consistent profitability, and a debt-light balance sheet.

It’s family controlled, but…

Chairwoman and CEO Ellen Gordon has been with the company for more than 60 years. Along with her family, she controls over 70% of the Class B shares, giving her near-total control. That’s not necessarily bad — some of the best companies are family-run — but in this case, it enables behaviors that are hard to square with long-term value creation.

Despite owning 33.5% of the market cap directly (~$543M), Gordon still collects a $7.2 million annual compensation package, including access to a corporate jet, chauffeur, and company apartment. Other executives receive cars and similar perks. For a low-growth candy company, this level of executive entitlement is difficult to justify.

Short-term mentality

Even though management presents itself as long-term focused, executive compensation is driven by short-term metrics. Annual performance goals include:

Growth in EPS

Growth in net earnings

Growth in sales of key brands

Cost savings

Acquisitions

And other “strategic” initiatives

These are goals that can be influenced quarter to quarter through cost-cutting, buybacks, or temporary marketing pushes — not by building durable value. There are no incentives tied to return on capital, for example.

We do not jeopardize long-term growth for immediate, short-term results.

Yeah, right…

Good capital allocation? Wait a sec…

The company holds $526.9 million in cash and investments (about 25% of market cap), mostly in short-term bonds and municipal securities. These are not opportunistic investments — they’re designed to fund future executive compensation obligations.

While the company does buy back stock — spending $13M–$33M per year since 2020 — those repurchases are being made at elevated valuations, not opportunistic discounts. With the stock trading nearly 3x above its intrinsic value, these buybacks are value-destructive, not accretive.

There’s no meaningful reinvestment in innovation, international expansion, or new brands. The capital is just... sitting there, or being spent on expensive stock and executive benefits.

EPS is growing, but…

Management points to EPS growth as evidence of consistent performance. But most of that growth has come from a declining share count, not improving fundamentals.

In other words, EPS is being inflated through financial engineering. Since revenues are largely flat, and margins haven’t meaningfully expanded, the only lever left is shrinking the denominator — not growing the numerator.

Problems with inventory disclosure

TR uses LIFO accounting for inventory — a defensible choice. But unlike peers such as Hershey, the company provides almost no transparency around how inventory is valued or managed.

No breakdown of inventory into raw materials, WIP, or finished goods

No LIFO reserve disclosure to compare with replacement cost

No write-downs or provisions for obsolete inventory — despite a clear trend of slower turnover (DIO increased from 56 to 81 days in 5y)

Meanwhile, Hershey, one of his closest peers, discloses all of this in detail — including the dollar impact of LIFO liquidations and inventory risk reserves.

Their minimal disclosures make it hard to assess whether inventory is overstated, aging, or subject to margin pressure. In a seasonal business, that opacity is a red flag in itself.

Problems with depreciation

The company depreciates machinery over up to 25 years and buildings over up to 40 years — assumptions that significantly understate annual depreciation and make operating income look stronger than it might be on an economic basis.

For comparison, Hershey Co., uses:

3 to 15 years for machinery and equipment

25 to 40 years for buildings

In other words, TR uses the upper end of the most aggressive assumptions, while Hershey applies more conservative and realistic depreciation to a more complex asset base.

The company also provides no detail on asset write-offs or depreciation policy reviews, making it harder for investors to assess whether capital reinvestment is being deferred or underreported.

Profits that don’t translate to cash

While TR generally posts positive operating cash flow, its cash conversion is inconsistent:

In 2022 and 2023, net income exceeded CFO — an unhealthy pattern for a mature business.

Only in 2024 did CFO exceed earnings, but largely due to non-cash adjustments and working capital swings.

In short: reported earnings don’t consistently convert to cash, which raises questions about the true economic power of the business.

Hidden pension risk

The company participates in a multi-employer pension plan for unionized workers — specifically the Central States Pension Fund, one of the most troubled in the country. As of the latest filings, the plan was only 47% funded and officially classified as “critical and declining.”

Normally, companies in such plans are exposed to something called withdrawal liability — essentially, if they pull out of the plan, they must cover their share of the unfunded obligations. For a company the size of Tootsie Roll, this could be substantial.

The only reason this hasn’t hit the balance sheet is because the plan was bailed out in 2021 with a $3.4B federal rescue under the American Rescue Plan Act. But let’s be clear:

That money went to the pension fund, not to Tootsie Roll.

It doesn’t erase Tootsie Roll’s exposure — it merely defers the problem.

If the plan deteriorates again, Tootsie Roll could be on the hook for additional contributions or withdrawal costs.

Unlike single-employer pensions, which must be fully reflected as liabilities on the company’s balance sheet, multi-employer pension obligations are off-balance sheet. That means shareholders can’t easily see the true scope of risk.

For a low-growth, low-margin company like Tootsie Roll, even a moderate pension call could weigh heavily on FCF.

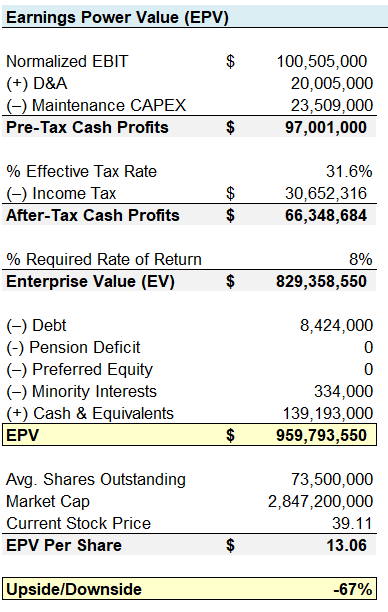

How much does TR worth?

On an Earnings Power Value (EPV) basis — which strips out growth assumptions and simply capitalizes normalized earnings — TR is worth about $$13/share

At today’s price of $39, that implies the stock is trading at nearly 3x its intrinsic value, or about 67% downside.

For a business with flat sales, weak reinvestment opportunities, and opaque accounting, this is a valuation that simply can’t be justified.

Conclusion

I started this research thinking I might write a traditional investment thesis on TR. What I found instead was a perfect case study in why investors need to dig deeper than the headline story.

On the surface, the company looks safe: iconic brands, no major debt, stable sales. But once you look closer, the red flags pile up:

Incentives tied to short-term metrics like EPS and net income growth

Buybacks at inflated prices that make EPS look better than it really is

Opaque accounting around inventory, depreciation, and cash flows

A hidden pension liability that doesn’t show up on the balance sheet

And a valuation that assumes growth where there is none

This doesn’t make TR a fraud, or even a bad company. But it does make it a bad stock at this price — and a great reminder that the details matter.

If all you look at is the brand and the balance sheet, you might think you’ve found a “safe company.” But if you study incentives, accounting choices, and capital allocation, you see the truth: this is a company where the long-term story doesn’t match the long-term reality.

That’s the real value of this exercise: Tootsie Roll isn’t just a stock to avoid — it’s a lesson in how to spot warning signs before you invest.

This is a superb analysis.