The Best Ideas I Found in Q2 2025 Investor Letters (Part IV)

From Alta Fox's investment thesis.

Did you miss the best ideas of Q1 2025?

No biggie, below you can download a PDF with 24 pages of the best ideas of Q1 2025 from investors letters

Also some best ideas of the Q2 2025

Investment thesis on

NCR Atleos (NYSE: NATL)

NCR Atleos (NYSE: NATL) – Alta Fox Capital

Alta Fox’s thesis on NCR Atleos centers on a straightforward but powerful disconnect between what the company is and how the market values it.

NATL is the clear leader in U.S. ATM outsourcing, with a market share in the mid-30% range and a dense nationwide servicing footprint. Its core “ATM-as-a-Service” model provides end-to-end cash access infrastructure for banks and credit unions, covering hardware procurement, software, regulatory compliance, cash handling, and maintenance. For financial institutions, outsourcing to NATL is a cost-saving, efficiency-improving move—reducing branch overhead while preserving or even expanding customer ATM access.

The competitive advantages are significant. NATL’s scale gives it purchasing power on ATM equipment, a more efficient logistics network for servicing machines, and the ability to amortize regulatory and compliance costs over a vast installed base. Switching costs are high: replacing an ATM outsourcing provider involves logistical disruption, regulatory re-approvals, and retraining internal teams. Regulatory complexity and entrenched contracts (often multi-year in length) further strengthen NATL’s moat. This infrastructure-heavy, contract-driven model results in roughly 70% of revenue being recurring and service-based, with low churn and predictable cash flows—features that resemble a transaction processing business more than a hardware vendor.

Why the Market is Wrong

Alta Fox argues that NATL’s valuation reflects a mistaken categorization as a low-growth, capital-intensive hardware business. In reality, the company’s economics are closer to those of a recurring service provider. CapEx are largely for maintenance rather than heavy growth builds, and FCF conversion is high. Once fixed servicing and infrastructure costs are covered, incremental revenue from new outsourcing deals or ATM placements flows disproportionately to the bottom line—a form of operating leverage often overlooked by investors.

This misunderstanding is compounded by investor bias against cash-dependent businesses, with some assuming that rising digital payments will lead to rapid ATM obsolescence. Alta Fox’s research suggests otherwise: while cash usage is slowly declining, it remains entrenched in certain geographies, demographics, and transaction types. Moreover, as banks consolidate branches, outsourcing ATMs becomes even more attractive as a way to maintain service coverage without physical branch costs. This trend will sustain NATL’s relevance for at least the next decade.

Valuation

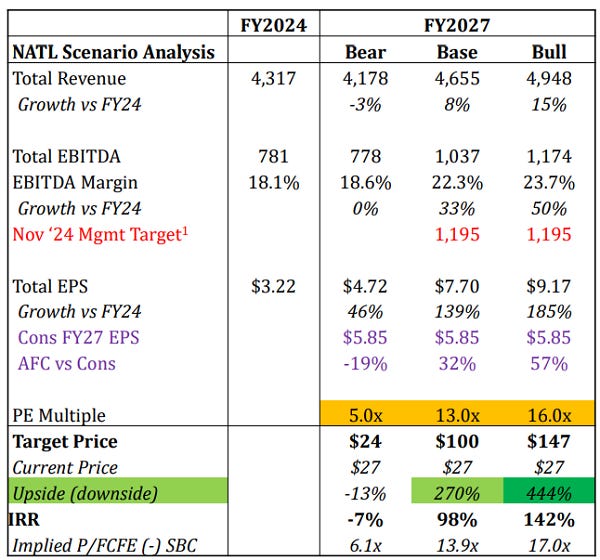

Base Case: ATMaaS conversions accelerate modestly, while the network business remains flat, leading to ~10% consolidated EBITDA growth per year. Debt paydown, buybacks, and lower cost of capital lift FY27 EPS to 32% above consensus, with a PE re-rating slightly below Diebold Nixdorf (DBD) levels. Target: $100/share (270% upside, ~98% IRR).

Bull Case: ATMaaS conversions hit management targets (~15% EBITDA CAGR), and the network business grows. PE re-rates to a premium over DBD to reflect NATL’s higher quality and faster growth. Target: $147/share (444% upside, ~142% IRR).

Bear Case: ATMaaS growth is only moderate, and network ATM counts decline mid-single digits annually. PE compresses to 5x. Target: $24/share (-13% downside, ~-7% IRR).

Catalysts

Growing investor recognition of NATL as a recurring revenue services platform

Increased ATM outsourcing penetration, especially among smaller banks and credit unions

Aggressive capital returns via buybacks and potential dividends

Debt reduction, lowering cost of capital

Potential M&A, either as acquirer or acquisition target for larger payment processors.

Risks

The primary risks are a faster-than-expected drop in cash usage, potential regulatory changes that negatively affect ATM economics, and execution challenges in maintaining service quality across such a large network. However, Alta Fox sees these risks as manageable, particularly given the contractual nature of much of NATL’s revenue and the gradual nature of payment preference shifts.

Conclusion

Alta Fox frames NATL as a **misunderstood, cash-generative infrastructure asset** masquerading as a hardware business in the eyes of the market. With stable recurring revenues, high free cash flow conversion, significant competitive advantages, and clear catalysts for a re-rating, NATL offers both downside protection and compelling upside potential. The firm believes that as investor perception shifts and capital allocation improves, NATL could see not only a higher multiple but also a sustained period of steady compounding.